The Introduction of the Open Banking System Will Develop the Domestic Financial Industry

▲ https://bit.ly/34EZmhr

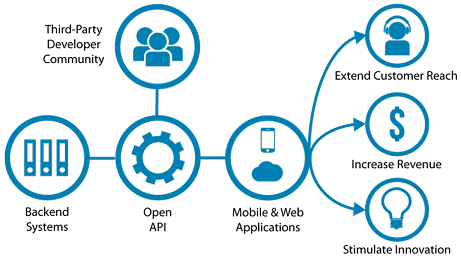

On October 30th, 10 domestic commercial banks launched the Open Banking system within their mobile Banking system. In December, eight additional banks, including Kakao Bank and Korea Development Bank (KDB), are expected to expand their mobile banking services as well. The Open Banking system is part of a financial technology system designed to meet three major conditions. First, using an Open API[1], the Open Banking system enables payment functions and customer data held by banks and other financial institutions to be used by third parties. Financial institutions can divide Open APIs by grade and provide different financial and management information for each grade. Therefore, financial institutions need to include only what they want to disclose in the API. Second, data contained in APIs, from open data to private data, should have financial transparency. Finally, open-source technology should be used as a means of achieving the formerly explained two conditions. In other words, financial institutions do not need to provide their own data sources. A third party only needs to use the information through an Open API. An Open Banking System that meets these conditions will allow companies developing financial technologies and financial customers to manage various bank accounts in a unified way. Nevertheless, the introduction of an Open Banking system has also brought concerning issues along with it because disclosure of financial information inevitably leads to security problems. As the pros and cons of the system clash, CAH decided to speculate on the views of both sides of the debate.

The Introduction of the Open Banking System Will Develop the Domestic Financial Industry

▲ https://bit.ly/2qaQzF4

Originally, the domestic Banking industry has been against providing Open APIs and applying open-source technology, both of which are key to the introduction of Open Banking. This is because each bank uses different security systems and issues different public certificates. Also, Korea's financial settlement network has been highly closed because of the usage of active x, which can only be supported by Internet Explorer browser. However, the growing demand for various web browsers and the distribution of MacOS systems, which are different from the Windows system, gradually opened up the closed financial settlement network. Open Banking is a business that started as part of this project. As mentioned before, currently the Opening Banking system is only applicable to 10 commercial banks. For now, the system is undergoing a trial operation. In the trial period only making use of other bank accounts through one application is functioned. On December 18th, the full Open Banking system will be introduced. Then, the fin-tech[2] firms will also form a new paradigm by gaining access to open-source. In this sense, speculation is needed to consider the potential positive effects which the introduction of Open Banking will present to the domestic market.

▲ https://bit.ly/2qakAVu

First, the introduction of the Open Banking will facilitate the development and delivery of new financial products. Before its introduction, the providers of the financial services had been limited to several small and medium-sized fin-tech firms. Conversely, the full introduction of the Open Banking system will allow every fin-tech firm to become the provider of financial products. Previously, fin-tech firms were heavily restricted from providing financial services. To launch fin-tech services, fin-tech firms had to sign agreements with each bank. In addition, there were difficulties in providing compatible fin-tech services to multiple banks because each bank had different data processing standards. Under the Open Banking system, however, this problem is solved because all banks share open-source and the Open API. In fact, 138 fin-tech firms have applied for Open Banking in advance, according to the Korea Financial Telecommunications & Clearings Institute (KFTC). Along with the market entry of these fin-tech firms, it is expected that personalized services will be developed using financial data obtained through Open API. As can be seen from the example of Open Banking in Europe, the introduction of Open Banking in Korea could boost the market for new financial products. Because there may be introduction of new services to manage customers' assets and spending through the fact that all banks' accounts will be linked.

Second, the introduction of Open Banking will contribute to the development of fin-tech firms. To start with, commission costs will reduce up to one-twentieth of the previous cost. Under the previous fee system, forwarding transfers cost 500 won and deposit transfers cost 400 won. This was consistent regardless of the size of the companies. However, if Open Banking is introduced, it will distinguish between large and small fin-tech firms (large firms being firms with monthly transactions of 10 billion won per month and firms with 100,000 transactions per month). In the case of large fin-tech firms, forwarding transfers will be reduced by one-tenth from 50 won to 40 won. In the case of small and medium-sized fin-tech firms, transaction fees will be reduced even more. Forwarding transfers will be 30 won and the deposit transfer will be 20 won. When compared to the existing transfer fees, the cost can be reduced by up to one-twentieth. The following cost reductions are possible in Open Banking because the technology allows fin-tech firms to depend less on banks. Previously, fin-tech firms had to demand original data from banks each time, but now firms will be able to use the information 'on their own' through Open API. This will reduce the cost. Also, M&A with various fin-tech firms will become important for banks in order to gain an upper hand in competition under the Open Banking system. Fin-tech firms will reduce development costs through collaboration with banks. With the introduction of Open Banking, fin-tech firms will be able to cut costs significantly, thereby allowing fin-tech firms to invest in better service. Overall, this will bring innovation to the financial industry in the long run.

Third, the introduction of Open Banking will improve convenience in ordinary financial transactions, as users will be able to manage their financial transactions at once. According to data released in March 2019 by the Bank of Korea, the number of customers registered for Internet Banking at local banks stood at 146.56 million by the end of 2018, compared with 16.07 million for mobile Banking. The figures also represent an 8.5 percent and 16.7 percent increase from the previous year. As such, there are so many people using either Internet or mobile Banking, and the number is rapidly increasing. Prior to the introduction of Open Banking, each user had to install applications individually or download different security systems used on each bank site. With the introduction of Open Banking, however, one can now manage all bank accounts though one account as long as one agrees to register. Even Banking services will become available through fin-tech firms' apps, not through banking services. Take, for example, Toss, a simple remittance service app, which has a cumulative download of more than 30 million and a cumulative number of about 13 million users. Through fin-tech apps like Toss, not only would simple remittance services be possible, customers would also be able to check all banks’ pension assets and to invest in financial products. To date, service users have had to download the online application to receive fin-tech services. However, under the new Open Banking system, fin-tech services will be available immediately through the existing Banking applications. In other words, through Open Banking, consumers will have easier access to finance with more options to choose from.

Open Banking has raised security concerns about financial information. However, according to the Financial Services Commission, only fin-tech firms that have passed security checks such as the Korea Financial Security Institute will be allowed to participate in Open Banking. This will prevent security issues in advance. It is clear that we need to pay constant attention to security issues. However, it is an anachronistic decision not to introduce Open Banking, which is expected to expand the entry of fin-tech firms, reduce unnecessary costs, improve financial convenience, and to innovate the financial industry. Therefore, the introduction of Open Banking is necessary.

[1] Abbreviated term for the Application Programming Interface: the system allows control of the functions provided by the operating system or programming language within the application.

[2] A term created from the mixture of “financial” and “technology;” the term also refers to changes in financial services and industries which have been caused by the fusion of finance and IT